Show summary Hide summary

Major Brazilian banks are moving to make satellite-based deforestation checks a routine part of lending for rural operations, a step that could reshape access to farm credit and intensify pressure on producers to meet environmental standards. The change reflects growing demand from investors, regulators and global buyers for finance that explicitly excludes recently deforested land.

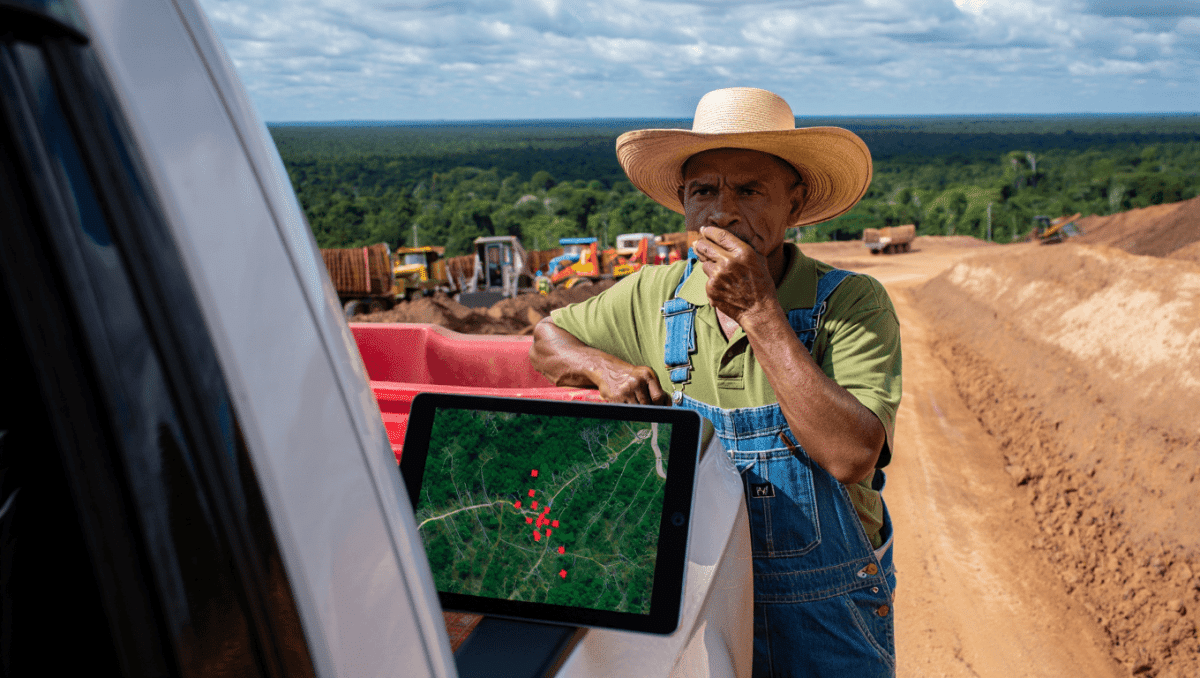

What the new checks mean in practice

Under the emerging approach, lenders will cross-reference applicants’ land with up-to-date satellite imagery before approving or renewing loans for agricultural production. The goal is to identify recent clearing or forest loss that would conflict with legal requirements or the banks’ own sustainability policies.

Verification will not rely on a single source. Financial institutions are expected to use a mix of publicly available maps, satellite data from commercial providers and national monitoring systems, and compare those images with declarations on land registries such as the Rural Environmental Registry (CAR).

England poised to end World Cup drought as Kane drives title push

Maine Democrats summon convention to pick Platner’s successor: senate race fallout

The practical outcome: applications tied to plots showing significant recent clearing may face additional review, conditions (such as restoration plans) or rejection. For lenders, the checks are intended to reduce reputational and regulatory risk; for borrowers, they add a new compliance step to access credit.

Checks banks will typically perform

- Confirm the absence of recent deforestation on parcels submitted for financing.

- Detect overlaps with protected areas, indigenous territories or conservation units.

- Compare satellite evidence with self-declared boundaries in the CAR and other records.

- Flag riverside vegetation and riparian buffers that should remain intact under environmental rules.

- Identify land-use changes after a defined cutoff date used by the lender’s policy.

These steps are designed to be scalable: they can be applied quickly to large portfolios using automated tools, while suspicious cases are escalated for on-the-ground verification.

Not every flagged parcel will automatically lose access to credit. Banks are likely to distinguish between historical, legitimate land use changes and recent, illegal clearing — but that assessment frequently requires follow-up work and, in some cases, legal clarification.

Why this is happening now

Market forces are a central driver. International buyers and asset owners increasingly demand deforestation-free supply chains, and some overseas lenders already screen agricultural finance for environmental risk. Domestically, tighter regulatory scrutiny and media attention on land-use change have raised the stakes for banks that finance rural markets.

For financial institutions, incorporating satellite checks is a way to standardize due diligence and respond to stakeholders pressing for more transparent risk management. It also aligns lending practices with broader climate and biodiversity commitments that many banks have publicly made.

Potential impacts and trade-offs

Farmers and ranchers will feel the effects unevenly. Medium and large producers who already use mapping and have formal land documentation are better positioned to pass rapid verifications. Smallholders and family farms, where records are more likely to be incomplete and technical capacity limited, risk delays or denials if support measures are not included.

Industry observers note the risk of unintended consequences: stricter screening without complementary technical and financial assistance could push some producers toward informal credit sources or increase disputes over land boundaries.

At the same time, proponents argue the measure could accelerate compliance and restoration efforts by linking finance directly to environmental outcomes — effectively using credit access as leverage to halt recent illegal clearing.

What stakeholders want to see next

Advocates for a balanced rollout emphasize three priorities: clear public rules about what constitutes disqualifying deforestation, transparent methodologies for satellite analysis, and targeted support for smallholders to meet requirements.

Without these elements, the new verification practices could widen gaps in financial inclusion. With them, banks say the checks will strengthen risk controls and help align Brazilian agriculture with global sustainability expectations.

Implementation timelines remain institution-specific. Some banks plan phased rollouts that begin with portfolio reviews; others may start applying checks at the point of new loan approvals. Whatever the pace, the move cements satellite monitoring as a permanent tool in agricultural finance and signals a tighter link between environmental compliance and access to credit in Brazil’s rural economy.